ATO patience runs out as small business tax debt hits $35b.

The recent news headline (you can read more here) confirms the increased collection activities being undertaken by the ATO. We know that managing ATO tax arrears can be challenging for businesses, especially with recent changes in recovery practices. As the ATO is increasing pressure to collect outstanding taxes, businesses need to be proactive in exploring all available options to manage debts effectively.

The Current State of Play:

The ATO’s approach to managing arrears has become more aggressive, especially for businesses with debts over $100,000.

The ATO is now:

- Registering defaults on company credit files for any “unaddressed” arrears over $100,000.

- Becoming less receptive to payment plans. If a payment plan is requested, the ATO now requires more detailed financial submissions for debts exceeding $200,000.

For businesses with arrears:

- Under $200,000: A 10% deposit is required, with a typical repayment term of 18 months.

- Over $200,000: A 10% deposit plus supporting financial information must be provided to secure a plan, making cash flow management more difficult.

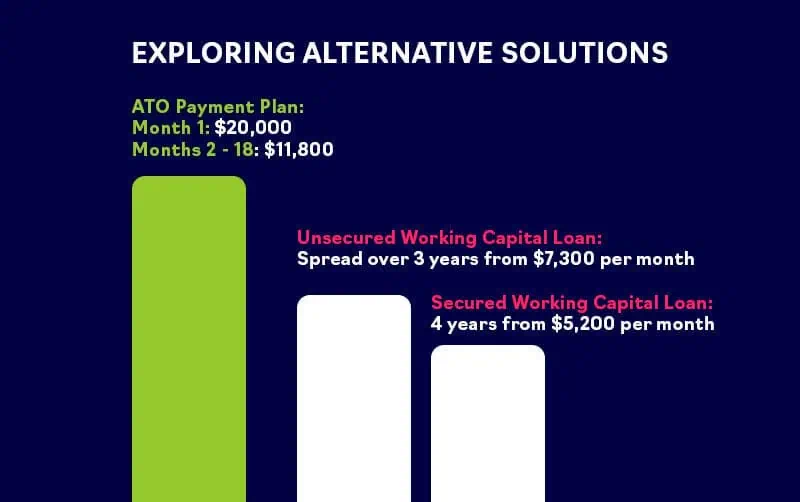

For a working example, on a $200,000 debt, a standard ATO payment plan might look like:

- Month 1: $20,000

- Months 2–18: $11,400

This shorter repayment schedule can create significant cash flow strain, limiting a business’s ability to operate smoothly.

Exploring Alternative Solutions

If a standard ATO payment plan isn’t feasible, businesses can explore alternative financing solutions such as unsecured or secured working capital loans. These options provide more flexible and manageable repayment schedules, helping businesses ease cash flow pressure.

Click here to learn more about how this can work for you and your business.

For the same $200,000 debt from above would look like the following:

- Unsecured Working Capital Loan: Spread over 3 years at $7,300 per month.

- Secured Working Capital Loan: Using unencumbered assets, this loan can be structured over 3 years at $6,575 per month or over 4 years at $5,200 per month.

These solutions can offer greater flexibility, allowing businesses to manage their finances without sacrificing operational stability.

Why Act Now?

Many businesses have successfully navigated ATO arrears by exploring bespoke finance solutions. Tailored repayment options can help reduce stress, improve cash flow, and provide the flexibility needed to keep operations running smoothly. Taking proactive steps now can ensure your business remains on track and positioned for growth.

Stay in the know! Follow Finlease on all social media platforms for the latest updates, tips, and insights.

More News

Financing Your First Excavator: A Guide for New Operators | Finlease

5 Things a Transparent Finance Broker Always Does | Finlease